-

Device Limitation: The app had to be restricted to devices provided by Utkarsh Bank.

-

Low/No-Network Functionality: Ensure the app’s functionality in remote areas with limited or no network connectivity..

-

Data Sync and Account Creation: Develop a mechanism to sync data with the central database and create accounts when network connectivity is available.

- Tailored Android App: Develop a secure and optimized Android app for Utkarsh Bank devices.

- Offline Functionality: Implement features for offline banking operations, including data caching.

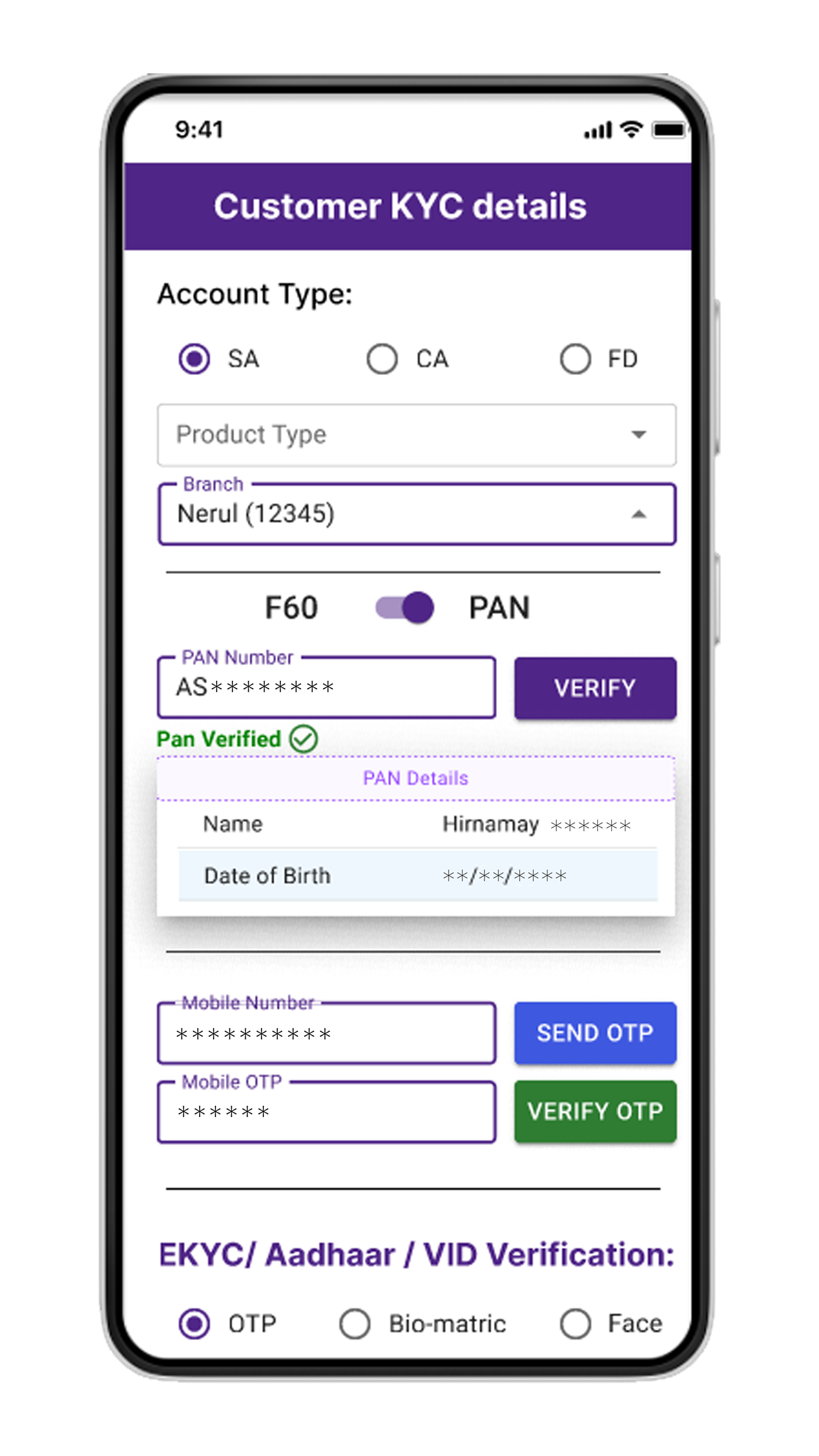

- Authentication and KYC Integration: Integrate multi-factor authentication and KYC processes for secure account opening.

- Data Synchronization: Develop a robust data sync mechanism for offline transactions.

- Tailored Android App Development:

-Fermion leveraged the latest Android technology to develop a custom mobile app, ensuring compatibility with the devices provided by Utkarsh Bank.

-The app was optimized for performance on restricted hardware, ensuring a seamless user experience for Utkarsh agents.

-

Network-Independent Functionality:

-Implemented features allowing the app to function in low/no-network areas, ensuring uninterrupted service in remote parts of the country.

-Developed an intelligent data caching mechanism to store transactions locally until a network connection was re-established.

- Authentication and KYC Integration:

-Implemented multiple levels of authentication to enhance security, including Aadhar verification and PAN card verification.

-Integrated KYC processes to streamline account opening procedures for Utkarsh agents.

- Data Sync and Account Creation:

-Developed a robust mechanism to sync data with the central database whenever a network connection was available.

Ensured that account creation processes were seamless, allowing Utkarsh Bank to expand its reach and open accounts efficiently.

- Successful App Deployment: The mobile app has been live since 2019, serving as a critical tool for Utkarsh Bank’s financial inclusion initiatives..

- Over 6 Lakh Accounts Opened: The app’s implementation has led to the successful opening of over 6 lakh accounts, underscoring its impact on Utkarsh Bank’s mission to reach remote communities.

- Efficient Remote Banking: Utkarsh agents can now conduct banking operations seamlessly in low/no-network areas, significantly enhancing financial services accessibility in remote regions.

- Accuracy Improvement: Over 10L accounts created till date for the remote area residents. 500+ Concurrent Agents work at the same time to make it possible.